Money Market Cash Hoard Origins, short rationale, LNG market expansion

Money Market Cash Hoard Origins

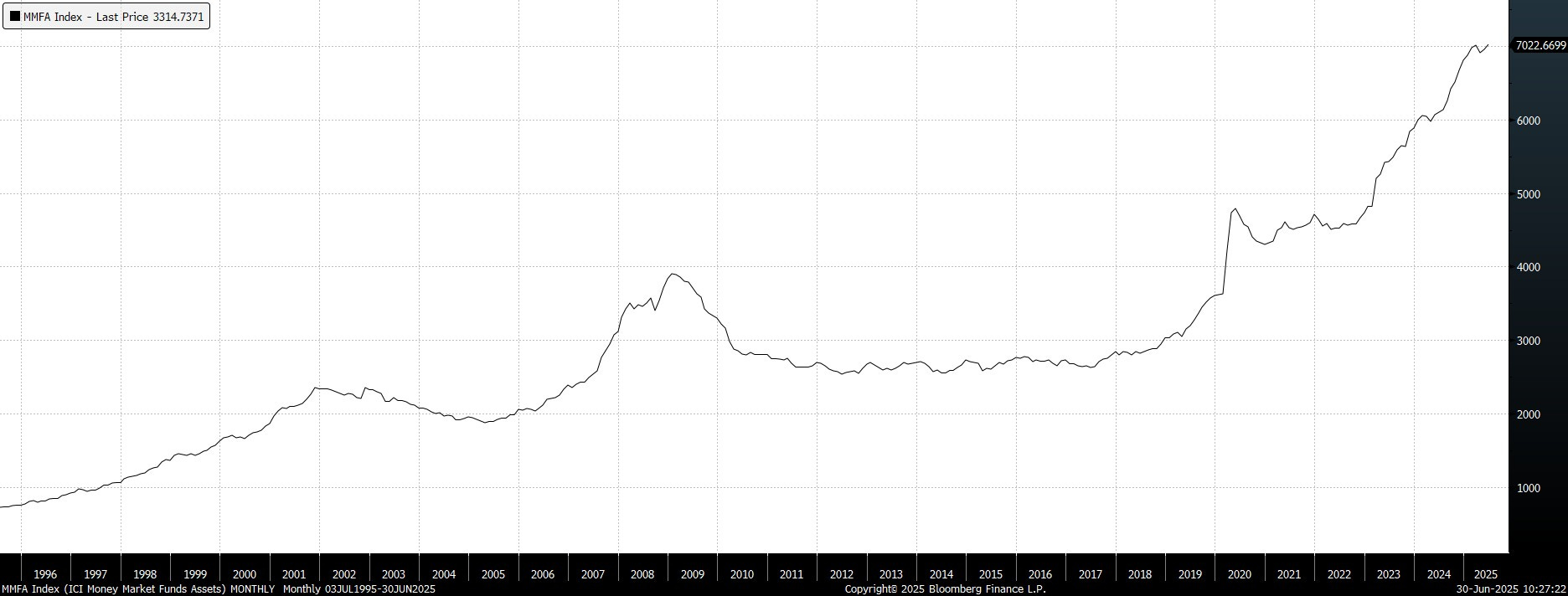

The volume of money committed to money market funds continues to climb. The headline number just passed $7 trillion.

The most basic assumption is if money is trending into money market funds, investors must have concluded that there is no better place to invest.

That’s hard to justify when stock markets are at new highs and bond yields are compressing.

Something else must be responsible for this extra $2 trillion that has been deposited in money market funds since early 2023.

I believe there are two partial answers that shed some light on this question.

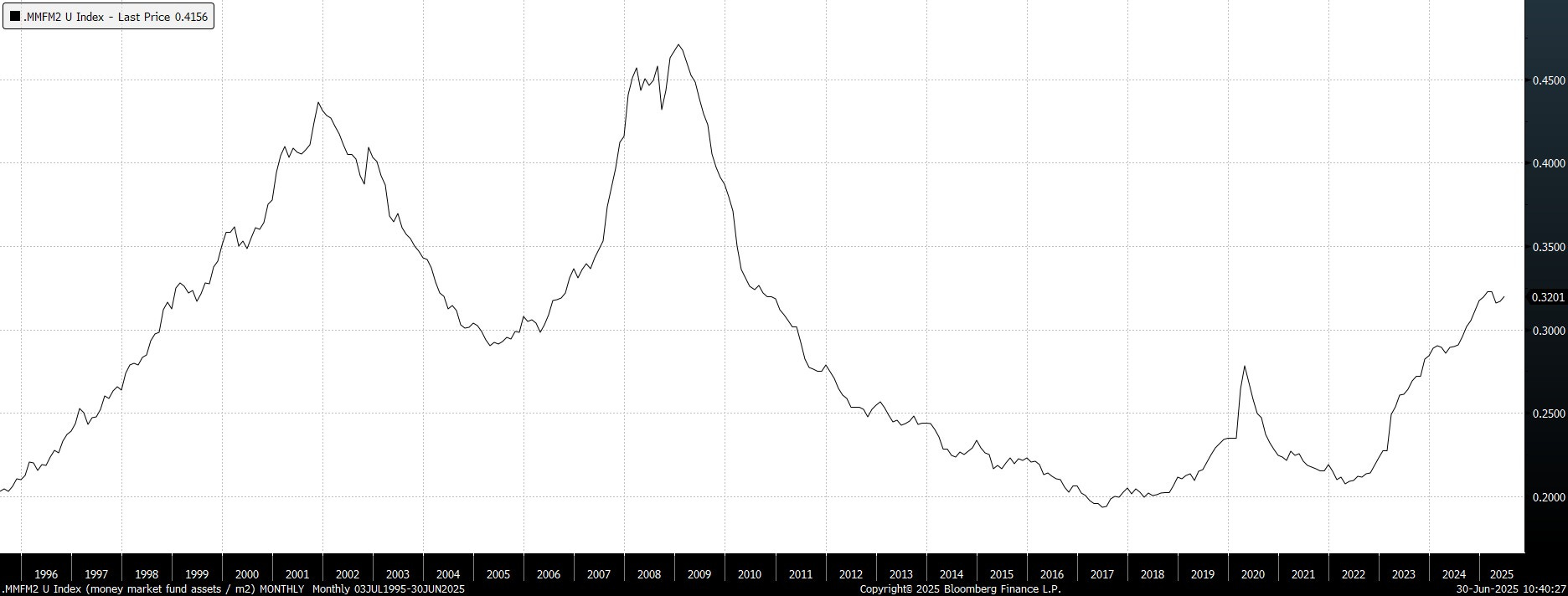

The first is that the cash committed to money markets funds is a normal percentage allocation as the supply of money increases. By this logic it is benefitting from the rise in asset prices more generally.

To test this hypothesis I created a ratio of money market funds total assets compared to M2.

The ratio provides some commonsense insights. Commitments of cash to money markets funds rise quicker than that money supply growth during economic expansions. They peak around the same time as interest rates and that tends to coincide with market peaks.

Between 2008 and 2017 the money market fund asset grew more slowly than M2 because rates were close to zero and there were better places to put cash to work.

The uptrend since 2022 can only be explained by rates. With the Fed Funds rates at 4.5% and a flat yield curve, investors have no clear incentive to embrace long-dated bonds.

Perhaps the most useful insight from this ratio is it trends lower when people need the cash for something else.

Between 2002 and 2005 rates dropped but institutions also needed cash due to redemption requests amid a stock market decline and economic uncertainty.

The slump between the 2008 peak and 2010 was largely for the same reason and the continued downtrend was probably because of QE and low rates.

The decline from the 2020 peak was driven by outsized money printing and fiscal excess that overwhelmed the move into money market funds.

So what about now?

The trend higher since 2022 is continuing at a quicker pace than money supply growth. In a normal cycle that would continue until the Federal Reserve aggressively cuts rates to combat emerging recession risk.

The combination of lower rates and the need for cash usually results in the ratio declining.

What about the 2nd reason?